Quoted from Empiritrage.com:

"We propose a model that is designed to identify bull-market and bear-market regimes. We examine correlation between stocks and bonds as a signal. Our hypothesis is that negative correlation between long bonds and stocks represents a bear-market regime, and a positive, or non-existent correlation, reflects a bull market regime.The model calculates rolling 90-day correlation estimates between the S&P 500 and long-bonds. At each month end, the model computes the 60-day MA of the correlation against the 600-day MA of the correlation. If positive, the model invests in risk; if negative, the model invests in riskless."

I will do a different kind of implementation so my results will differ due to different data and different strategy. When referring to correlation I will be referring to the correlation of the SP500 to the inverse of the 10-year Treasury yield.

The system will either be long the SP500 or be in cash.

Each month it will look at the short and long term correlations and if stocks/bonds tend to be more correlated than usual, it buys the SP500. If not, it sells it and holds cash.

I will be using yahoo free data: ^GSPC (S&P500 Index) data as the "risk" asset and (1/ ^TNX, the reverse of the 10-year Treasury Yield) to represent long-bonds.

The above graph is using params [90,60]

Just for fun let's do the exact opposite: We will buy when the short term correlation is less than the long term one. Same parameters.

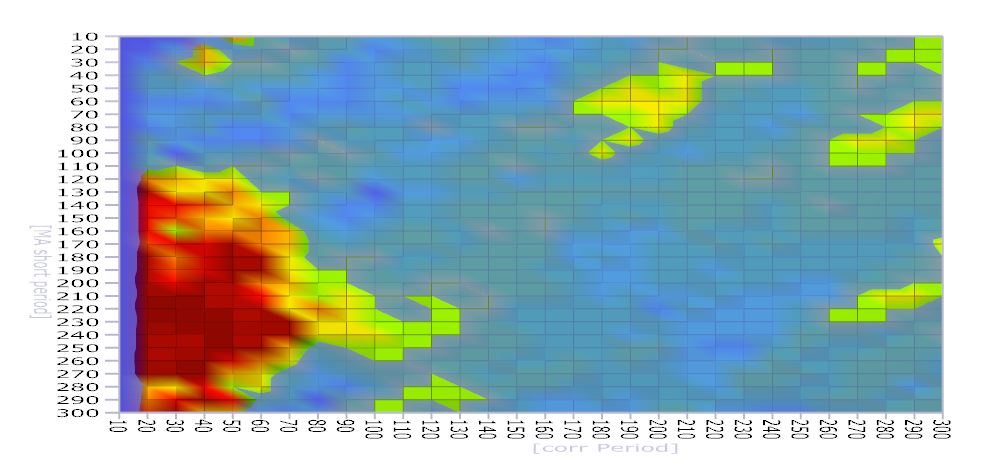

Let us optimize the parameters to get a better sense of what is happening. Is there a "general acceptable area"?

params: [10-->300 10-->300]

Using these optimized parameters, what would trading the 5 core etfs would look like? Risk on means buy SPY,EEM,EFA and VNQ. Risk off means buy IEF.

The equity is for the whole 5 -asset system. The lower pane shows the Emerging Markets time series (NYSEARCA:EEM).

You can see from the lower graph, this system did not buy EEM for the whole 2010-2013 period.

Going back to just trading the SP500, what would happen if we added the simple MA rule. Buy as before but only if price is above it's 200-day moving average. Sell as before but also sell if price is less than it's 200 moving average:

Disclaimer: This is a quick and dirty try-out of whether stock/bond correlation can help differentiate bull/bear regimes. It's not meant to be precise but rather to get you started in performing your own tests.

Few thoughts on TAA:

I will caution the reader that when it comes to "TAA" strategies, for the past few years, holding both the S&P500 (SPY) and bonds (IEF) was an exceptional strategy whether you timed it or not. That is mostly due to the fact that IEF, the 10-year treasury proxy had both an exceptional run and a fairly uncorrelated one to the stock index. As others have mentioned, TAA systems may have a hard time delivering if Treasury yields stop dropping (below zero..?). But one way to look at the typical TAA strategy is that it is a diversified "short-the-dollar" strategy. Looking at it that way, there is room to diversify to non -U.S. denominates assets.

The code in Amibroker:

I will be using yahoo free data: ^GSPC (S&P500 Index) data as the "risk" asset and (1/ ^TNX, the reverse of the 10-year Treasury Yield) to represent long-bonds.

We 'll keep 2 parameters optimizable and lock the long moving average period to 600, to keep things simple.

Params [90,60]

a. CorelationPeriod (default=90)

b. MAshortPeriod (default=60)

risk=Foreign("^GSPC","C");

bond=1/Foreign("^TNX","C");

Corr=Correlation(risk,bond,CorelationPeriod);

Buy=MoreCorrelated=MA(Corr,MAshortPeriod )>MA(Corr,600);

Just for fun let's do the exact opposite: We will buy when the short term correlation is less than the long term one. Same parameters.

params: [10-->300 10-->300]

There seems to be a "better" area of settings than the one we are using.

Let's try the backtest with params [40 220]. In other words we are calculating correlation using a 2-month window. We are then comparing the almost yearly moving average of that to the 600-day longer term one.

Using these optimized parameters, what would trading the 5 core etfs would look like? Risk on means buy SPY,EEM,EFA and VNQ. Risk off means buy IEF.

The equity is for the whole 5 -asset system. The lower pane shows the Emerging Markets time series (NYSEARCA:EEM).

You can see from the lower graph, this system did not buy EEM for the whole 2010-2013 period.

Going back to just trading the SP500, what would happen if we added the simple MA rule. Buy as before but only if price is above it's 200-day moving average. Sell as before but also sell if price is less than it's 200 moving average:

Disclaimer: This is a quick and dirty try-out of whether stock/bond correlation can help differentiate bull/bear regimes. It's not meant to be precise but rather to get you started in performing your own tests.

Few thoughts on TAA:

I will caution the reader that when it comes to "TAA" strategies, for the past few years, holding both the S&P500 (SPY) and bonds (IEF) was an exceptional strategy whether you timed it or not. That is mostly due to the fact that IEF, the 10-year treasury proxy had both an exceptional run and a fairly uncorrelated one to the stock index. As others have mentioned, TAA systems may have a hard time delivering if Treasury yields stop dropping (below zero..?). But one way to look at the typical TAA strategy is that it is a diversified "short-the-dollar" strategy. Looking at it that way, there is room to diversify to non -U.S. denominates assets.

The code in Amibroker:

/

/----Code by Sanz P.-----------------------------------------------------// newMonth=Month()!=Ref(Month(),-1); MAperiods=Param("MA Periods",200,100,400,5); AboveMA=C>MA(C,MAperiods); BelowMA=C<MA(C,MAperiods); spy=Foreign("^GSPC","C"); ief=1/Foreign("^TNX","C"); Corrperiod=Optimize("corr Period",40,10,300,10); MAshort=Optimize("MA short period",220,10,300,10); Corr=Correlation(spy,ief,Corrperiod); MoreCorrelated=MA(Corr,MAShort)>MA(Corr,600); if(Name()=="^GSPC") { Buy=MoreCorrelated AND newmonth;// AND abovema; Sell=(!MoreCorrelated /*OR !abovema*/) AND newmonth; } /* if(Name()=="IEF") { Buy=!MoreCorrelated AND newmonth ; Sell=MoreCorrelated AND newmonth; } */ PosQty =Param("How many Positions",1,1,20,1); SetOption("MaxOpenPositions", PosQty ); SetTradeDelays(0,0,0,0); BuyPrice=SellPrice=C; PositionSize=-96/PosQty ;